Factor Based Analysis

In the previous two posts we learned how to download and clean the Fama French 3 factors data. In this post we will use those factors to analyze mutual funds performance.

But before we proceed let us understand what Fama French factor model really is.

The traditional asset pricing model (CAPM), used only one factor (Market returns) to explain the returns of a portfolio or a stock. Fama & French concluded that CAPM model was not sufficient to explain all the sources of returns for a portfolio. Their observation and research led to the conclusion that portfolios built using small cap stocks that have a low price to book ratio (value stocks), tend to do better than market portfolios. Over time they have added many more factors such as momentum, operating profitability and conservative/aggressive portfolios.

But in this post we will look at their most famous 3 factors model to assess mutual fund managers performance.

Before Fama French’s research and data, most managers were evaluated based on their 5,10 or 20 years of performance. If a manager outperformed his/her benchmark they got more money to manage and a hefty fees. But such analysis will only show part of the whole picture.

Unless we do further analysis we wont know if the manager’s performance was due to luck, or a style tilt or genuine security selection skills.

To separate the wheat from the chaff, we need to regress the portfolio manager’s returns with common risk factors that are known to have outperformed in the past. And if the manager has a high exposure to such factors, we can replicate their portfolio at a cheaper cost using a factor based ETF.

This is the current debate on Wall Street. Active managers insist they posses extraordinary skills and therefore deserve the higher fees. Investors such as pension funds and endowments, take the other side and are increasingly allocating money to passive index funds, that provide exposure to these common factors.

So with this brief explanation out of the way we will analyze some mutual funds and their performance in light of Fama French 3 factors.

We will follow the below steps to analyze our mutual fund.

- Download & clean the Fama French 3 factors data

- Download the mutual fund price data

- Calculate the mutual fund’s returns data

- Combine both data sets & run regression analysis

- Analyze the results

So lets start and load our libraries

library(tidyquant)

library(timetk)Download Fama French Data

Because we will be downloading and cleaning our Fama French data many times, we will automate this step and build a function. This way we won’t have to repeat the steps for our analysis each time we analyze a new fund.

So lets build our function. The steps are all similar to what we did in the past. We are just wrapping those steps in a function.

# Automate Getting Fama French data from the website

get_fama_french <- function() {

#This is the URL for the website

ff_url <- "https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/ftp/F-F_Research_Data_Factors_CSV.zip"

# Create a temp file to store the data

temp_file <- tempfile()

# Download the data

download.file(ff_url, temp_file,quiet = TRUE)

# Unzip & Read the data

ff_data_raw <- read_csv(unzip(temp_file), skip = 3)

# This step is to delete the extra data that is not needed

# We are getting the row index where the data ends

ff_row <- which(is.na(ff_data_raw$SMB))

ff_row <- ff_row[1]

# Selecting only the rows we need for our analysis

ff_data_raw <- ff_data_raw[c(1:(ff_row - 1)),]

# Changing the Column names

colnames(ff_data_raw) <- paste(c('date', "mkt_excess", "smb", "hml", "rf"))

# Formatting the date column

# We want the end of the month dates

ff_data_raw <- ff_data_raw %>%

mutate(date = ymd(parse_date(date, format = "%Y%m"))) %>%

mutate(date = date + months(1)) %>% # Add one month

mutate(date = rollback(date)) # change it back to end of the month

# Finally converting the data from percent to decimal

ff_data_raw <- ff_data_raw %>%

mutate_at(vars(-date), function(x) x/100)

return(ff_data_raw)

}Now that we have built the function to get Fama French data automatically, lets test it.

ff_data <- get_fama_french()head(ff_data)## # A tibble: 6 x 5

## date mkt_excess smb hml rf

## <date> <dbl> <dbl> <dbl> <dbl>

## 1 1926-07-31 0.0296 -0.023 -0.0287 0.0022

## 2 1926-08-31 0.0264 -0.0140 0.0419 0.0025

## 3 1926-09-30 0.0036 -0.0132 0.0001 0.0023

## 4 1926-10-31 -0.0324 0.0004 0.0051 0.0032

## 5 1926-11-30 0.0253 -0.002 -0.00350 0.0031

## 6 1926-12-31 0.0262 -0.0004 -0.0002 0.0028tail(ff_data)## # A tibble: 6 x 5

## date mkt_excess smb hml rf

## <date> <dbl> <dbl> <dbl> <dbl>

## 1 2018-12-31 -0.0955 -0.0258 -0.0151 0.0019

## 2 2019-01-31 0.0841 0.0302 -0.006 0.0021

## 3 2019-02-28 0.034 0.0202 -0.0284 0.0018

## 4 2019-03-31 0.011 -0.0315 -0.0407 0.0019

## 5 2019-04-30 0.0396 -0.017 0.0198 0.0021

## 6 2019-05-31 -0.0694 -0.0125 -0.0238 0.0021We can see that data has been downloaded properly and just for sanity check we should plot it.

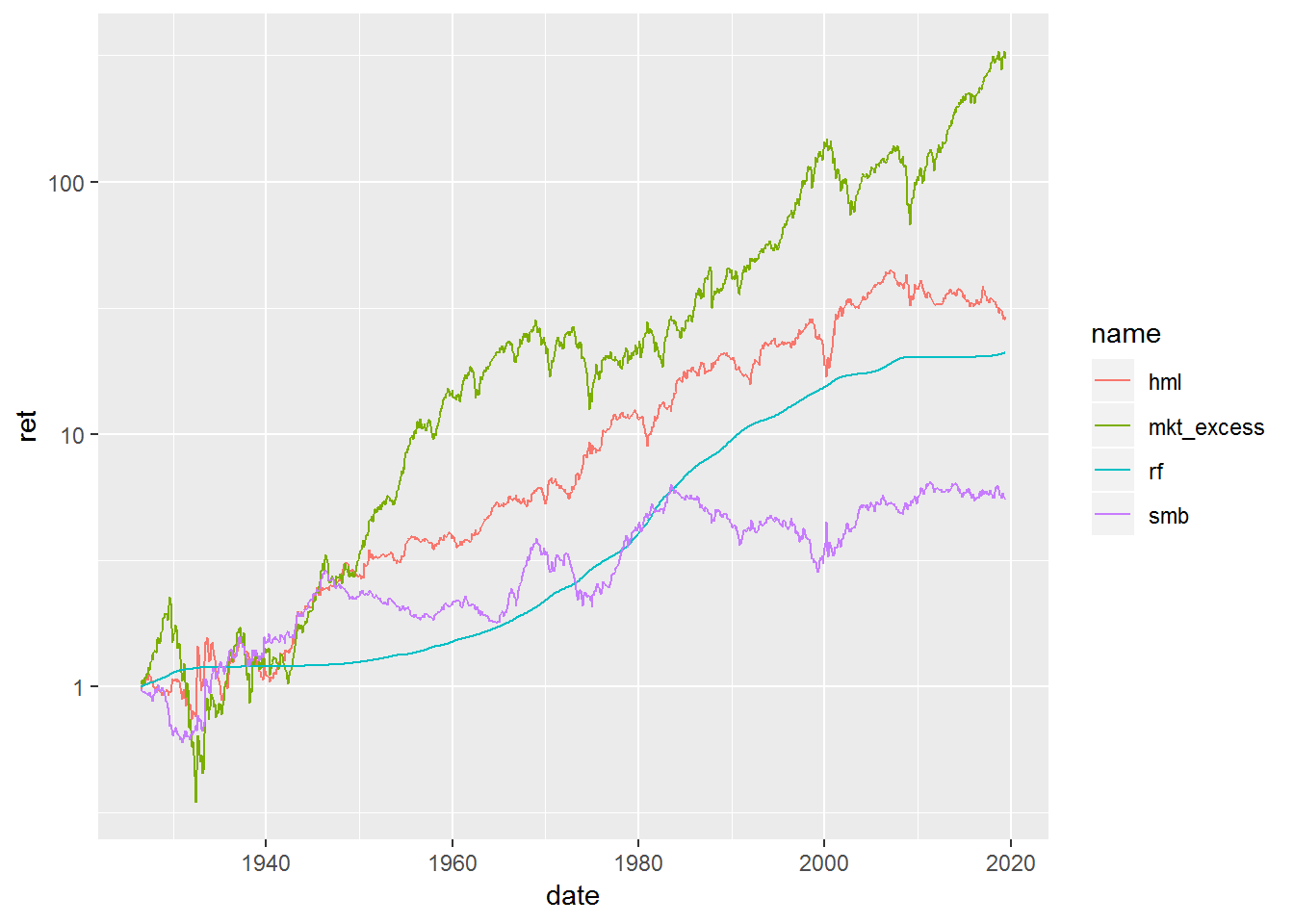

ff_data %>%

gather(mkt_excess:rf, key = name, value = val) %>%

group_by(name) %>%

mutate(ret = cumprod(1 + val)) %>%

ggplot(aes(x = date, y = ret, color = name)) +

geom_line() +

scale_y_log10()

The plot confirms that the data has been downloaded correctly. We see no spikes or dips in our time series.

Download the Mutual Fund Data

Next lets choose a mutual fund to analyze. For this exercise we wanted to choose an active mutual fund that has been managed for a long time. The size of the mutual fund also needs to be large. So we selected the Fidelity Contrafund Fund (FCNTX). The fund has data going as far back as 1980.

So lets download the data for the fund. Again we want to automate the process of downloading the price data for funds, this will accelerate our process and we will spend more time in analyzing the result versus downloading the data. We will build another function to do that.

# Type the ticker name

ticker <- "FCNTX"

# So this function requires the ticker, start and end date

# as arguments

get_price_data <- function(ticker, start, end) {

price_data <- tq_get(ticker,

from = start,

to = end,

get = 'stock.prices')

return(price_data)

}Now lets test our function.

# Type the ticker name

ticker <- "FCNTX"

# Start date

start <- "1980-01-01"

# End Date since we have FF data only till May

end <- "2019-05-31"

# Download the price

price_data <- get_price_data(ticker, start, end)Again lets plot it to make sure the data has been downloaded correctly.

price_data %>%

ggplot2::aes(date, adjusted) +

geom_line()## NULLhead(price_data)## # A tibble: 6 x 7

## date open high low close volume adjusted

## <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 1980-01-02 1.14 1.14 1.14 1.14 0 0.169

## 2 1980-01-03 1.12 1.12 1.12 1.12 0 0.167

## 3 1980-01-04 1.14 1.14 1.14 1.14 0 0.170

## 4 1980-01-07 1.14 1.14 1.14 1.14 0 0.169

## 5 1980-01-08 1.17 1.17 1.17 1.17 0 0.174

## 6 1980-01-09 1.17 1.17 1.17 1.17 0 0.174tail(price_data)## # A tibble: 6 x 7

## date open high low close volume adjusted

## <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 2019-05-22 12.8 12.8 12.8 12.8 0 12.8

## 2 2019-05-23 12.6 12.6 12.6 12.6 0 12.6

## 3 2019-05-24 12.6 12.6 12.6 12.6 0 12.6

## 4 2019-05-28 12.6 12.6 12.6 12.6 0 12.6

## 5 2019-05-29 12.5 12.5 12.5 12.5 0 12.5

## 6 2019-05-30 12.5 12.5 12.5 12.5 0 12.5Calculate the Returns Data

Next we will build another function that calculates the returns for our fund. Now we could have easily combined the function to download the price and calculate the returns together. But this is not a good programming practice. In general we want our functions (automation) to do one thing only. This makes it very easy to debug our programs.

So lets calculate the returns

# Automating the returns calculation

# We need to provide the price data table

# And the period, by default is monthly

# Since FF data is monthly

get_return_data <- function(closing_price, period = "monthly") {

# This step check to see if there are more than 1 tickers

is_symbol <- "symbol" %in% colnames(closing_price)

# If we have more tickers then we will use groupby()

if (is_symbol == TRUE) {

ret_data <- closing_price %>%

group_by(symbol) %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = period,

col_rename = 'returns')

return(ret_data)

# If we have only 1 tickers, we don't use groupby()

} else {

ret_data <- closing_price %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = period,

col_rename = 'returns')

return(ret_data)

}

}Lets use our function to calculate the returns

ret_data <- get_return_data(price_data,"monthly")head(ret_data)## # A tibble: 6 x 2

## date returns

## <date> <dbl>

## 1 1980-01-31 -0.00968

## 2 1980-02-29 -0.0169

## 3 1980-03-31 -0.0894

## 4 1980-04-30 0.0179

## 5 1980-05-30 0.0789

## 6 1980-06-30 0.0117tail(ret_data)## # A tibble: 6 x 2

## date returns

## <date> <dbl>

## 1 2018-12-31 -0.0804

## 2 2019-01-31 0.0945

## 3 2019-02-28 0.0240

## 4 2019-03-29 0.0221

## 5 2019-04-30 0.0488

## 6 2019-05-30 -0.0442Combine the data and run Regression

Once again we will build a function to combine the data and then another function that runs the multiple regression model on our data.

# We want the data to match the last day of our FF date

last_month_ff <- ff_data %>%

select(date) %>%

slice(nrow(ff_data)) %>%

.[[1]]

# Join the portfolio data with FF data

join_data <- function(ret_data, ff_data) {

joined_data <- ret_data %>%

filter(date <= last_month_ff) %>%

mutate(date = rollback(date, roll_to_first = TRUE)) %>%

mutate(date = date + months(1)) %>%

mutate(date = rollback(date)) %>%

left_join(ff_data,by = 'date') %>%

mutate(port_excess = returns - rf)

return(joined_data)

}Now lets see if the data was joined correctly.

ff_data <- join_data(ret_data,ff_data)head(ff_data)## # A tibble: 6 x 7

## date returns mkt_excess smb hml rf port_excess

## <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 1980-01-31 -0.00968 0.0551 0.0165 0.018 0.008 -0.0177

## 2 1980-02-29 -0.0169 -0.0122 -0.0182 0.0062 0.0089 -0.0258

## 3 1980-03-31 -0.0894 -0.129 -0.0664 -0.0106 0.0121 -0.102

## 4 1980-04-30 0.0179 0.0397 0.0097 0.0106 0.0126 0.00526

## 5 1980-05-31 0.0789 0.0526 0.0216 0.0039 0.0081 0.0708

## 6 1980-06-30 0.0117 0.0306 0.0167 -0.0089 0.00610 0.00564tail(ff_data)## # A tibble: 6 x 7

## date returns mkt_excess smb hml rf port_excess

## <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 2018-12-31 -0.0804 -0.0955 -0.0258 -0.0151 0.0019 -0.0823

## 2 2019-01-31 0.0945 0.0841 0.0302 -0.006 0.0021 0.0924

## 3 2019-02-28 0.0240 0.034 0.0202 -0.0284 0.0018 0.0222

## 4 2019-03-31 0.0221 0.011 -0.0315 -0.0407 0.0019 0.0202

## 5 2019-04-30 0.0488 0.0396 -0.017 0.0198 0.0021 0.0467

## 6 2019-05-31 -0.0442 -0.0694 -0.0125 -0.0238 0.0021 -0.0463We can see that the data has been joined correctly and now the final step is to run the regression model.

We will build a function to run the regression analysis.

# We need the boom package to tidy our data

library(broom)

# Multiple regression Analysis

run_reg_model <- function(ff_data) {

# Checks to see if we have more than 1 symbol

is_symbol <- "symbol" %in% colnames(ff_data)

if (is_symbol == TRUE) {

# Running the regression model

model <- ff_data %>%

nest(-symbol) %>% # Nesting the data and running the regression

mutate(model = map(data, ~lm(port_excess ~ mkt_excess + smb + hml, data = .))) %>%

mutate(model = map(model,tidy)) %>% # Cleaning the data results

unnest(model) %>% # Unnesting the data

mutate_if(is.numeric, funs(round(.,10))) # Rounding the results

return(model)

# Repeating the same steps for a single ticker

} else {

model <- ff_data %>%

nest() %>%

mutate(model = map(data, ~lm(port_excess ~ mkt_excess + smb + hml, data = .))) %>%

mutate(model = map(model,tidy)) %>%

unnest(model) %>%

mutate_if(is.numeric, funs(round(.,10)))

return(model)

}

}Now lets run the regression

model_data <- run_reg_model(ff_data)head(model_data)## # A tibble: 4 x 5

## term estimate std.error statistic p.value

## <chr> <dbl> <dbl> <dbl> <dbl>

## 1 (Intercept) 0.00112 0.00100 1.12 0.265

## 2 mkt_excess 0.888 0.0234 37.9 0

## 3 smb 0.0301 0.0345 0.873 0.383

## 4 hml -0.110 0.0357 -3.07 0.00227We have successfully run the regression model, before we continue let us show you the steps once again in case we need to analyze another fund. This is assuming you have already built all the functions, as explained above.

# Download the Fama French Data

ff_data <- get_fama_french()

# Set the ticker name

ticker = "FCNTX"

# Set the start date

start = "1980-01-01"

# Set the end Date

end = "2019-06-29"

# Download the price

price_data <- get_price_data(ticker, start, end)

# Get the returns

ret_data <- get_return_data(price_data, period = "monthly")

# Join the data

ff_data <- join_data(ret_data = ret_data,

ff_data = ff_data)

# Run the regression Model

model_data <- run_reg_model(ff_data = ff_data)Now lets analyze the regression data

print(model_data)## # A tibble: 4 x 5

## term estimate std.error statistic p.value

## <chr> <dbl> <dbl> <dbl> <dbl>

## 1 (Intercept) 0.00108 0.001000 1.08 0.282

## 2 mkt_excess 0.889 0.0234 37.9 0

## 3 smb 0.0304 0.0344 0.884 0.377

## 4 hml -0.108 0.0357 -3.03 0.00259Lets first look at the Intercept. This value is the alpha generated by fund controlling for market ,size and value factors. The fund appears to have generated an alpha of 0.0010773 per month. This suggests an alpha of 0.0130043 per year. However the p-value suggests that this is statistically not significant. The market factor is 0.88, most traditional equity funds have market exposure close to 1. This fund is marketed as a Large Cap growth fund. However, it appears to have some positive exposure to small cap factor, although p-value is not significant. Then finally, the fund has a negative exposure to the value factor, this makes sense since it is a large cap growth fund and invests in stocks such as Amazon, SaleForce, Facebook and Netflix which are high growth stocks.

This fund has generated returns above 12.5% since its inception in 1967. This is a remarkable track record for a very long time. US stocks have returns roughly 10% over that same period. The expense ratio/fees are around 0.82%, not too expensive. Many 401K plans offer this fund as an investment option. Past returns are no guarantee for future returns and this outperformance may disappear in the future.

This was a simple example to demonstrate how to

- Automatically download Fama French data

- Get the fund data

- Calculate the returns

- Run regression and analyze the results

Before we leave lets test all our functions on another fund.

We will choose another fund to check that all our functions are running properly. Let’s choose Goldman Sachs Strategic Growth A (GGRAX). This is a US Large Cap growth equity fund and has been in business since 1999.

So lets us demonstrate how we can automate our workflow in a single function.

This function combines all our above functions. This one function will download the price, calculate the returns, join the data and run the regression analysis.

# All data function

# We need to provide the ticker and start and end date for our fund data.

all_data_func <- function(ticker, start,end) {

ticker <- ticker

# Gets the FF data

ff_data <- get_fama_french()

# Gets the Price data

price_data <- get_price_data(ticker, start = start, end = end)

# Calculates the returns data

ret_data <- get_return_data(price_data, period = "monthly")

# Joins the data

all_data <- join_data(ret_data = ret_data,

ff_data = ff_data)

# Runs the regression model

model <- run_reg_model(all_data)

# Return the data

return(model)

}

goldman_fund <- all_data_func("GGRAX",

start = "1999-05-01",

end = "2019-06-30")print(goldman_fund)## # A tibble: 4 x 5

## term estimate std.error statistic p.value

## <chr> <dbl> <dbl> <dbl> <dbl>

## 1 (Intercept) -0.0000967 0.000802 -0.121 0.904

## 2 mkt_excess 1.02 0.0188 54.3 0

## 3 smb -0.187 0.0254 -7.34 0

## 4 hml -0.171 0.0259 -6.58 0.0000000003Great news!!! This works as expected.

In the next post we will scrape mutual fund data and analyze multiple portfolios using Fama French 3 factor Models.